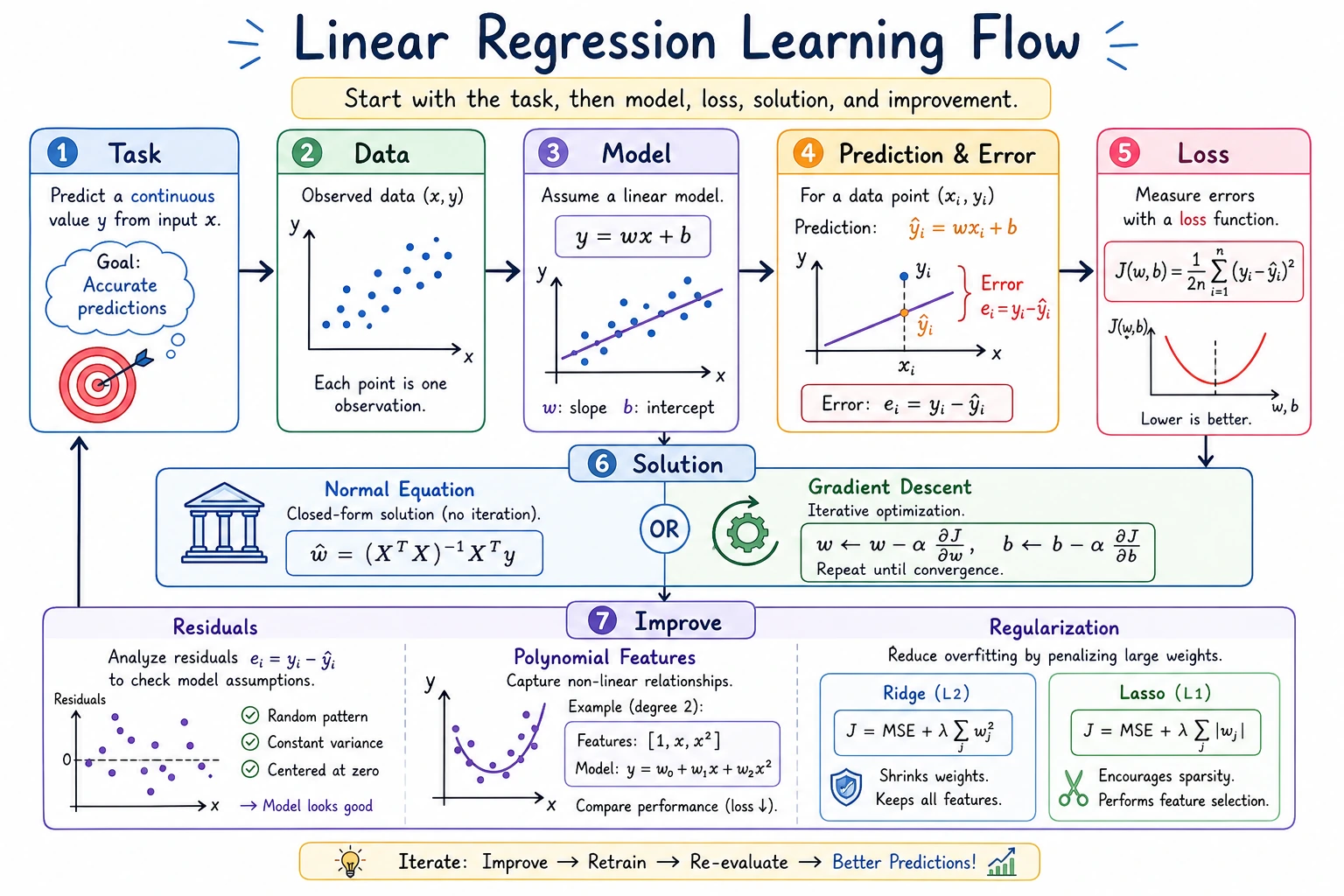

5.2.2 Linear Regression: Baseline, Residuals, Regularization

Linear regression answers one practical question: can a few input numbers explain or predict one continuous target number? Examples: price, sales, demand, temperature, latency, or cost.

Look at the Intuition First

Section titled “Look at the Intuition First”

Keep this mental model:

| Word | First meaning |

|---|---|

| feature | an input column such as area, rooms, age |

| coefficient | how much the prediction changes when one feature increases |

| intercept | the base prediction before feature effects are added |

| residual | true value - predicted value |

| RMSE | typical error size, penalizing large misses |

| MAE | typical absolute error, easier to explain |

| R² | rough percentage of variation explained by the model |

Run the Complete Regression Lab

Section titled “Run the Complete Regression Lab”Create ch05_linear_regression_lab.py.

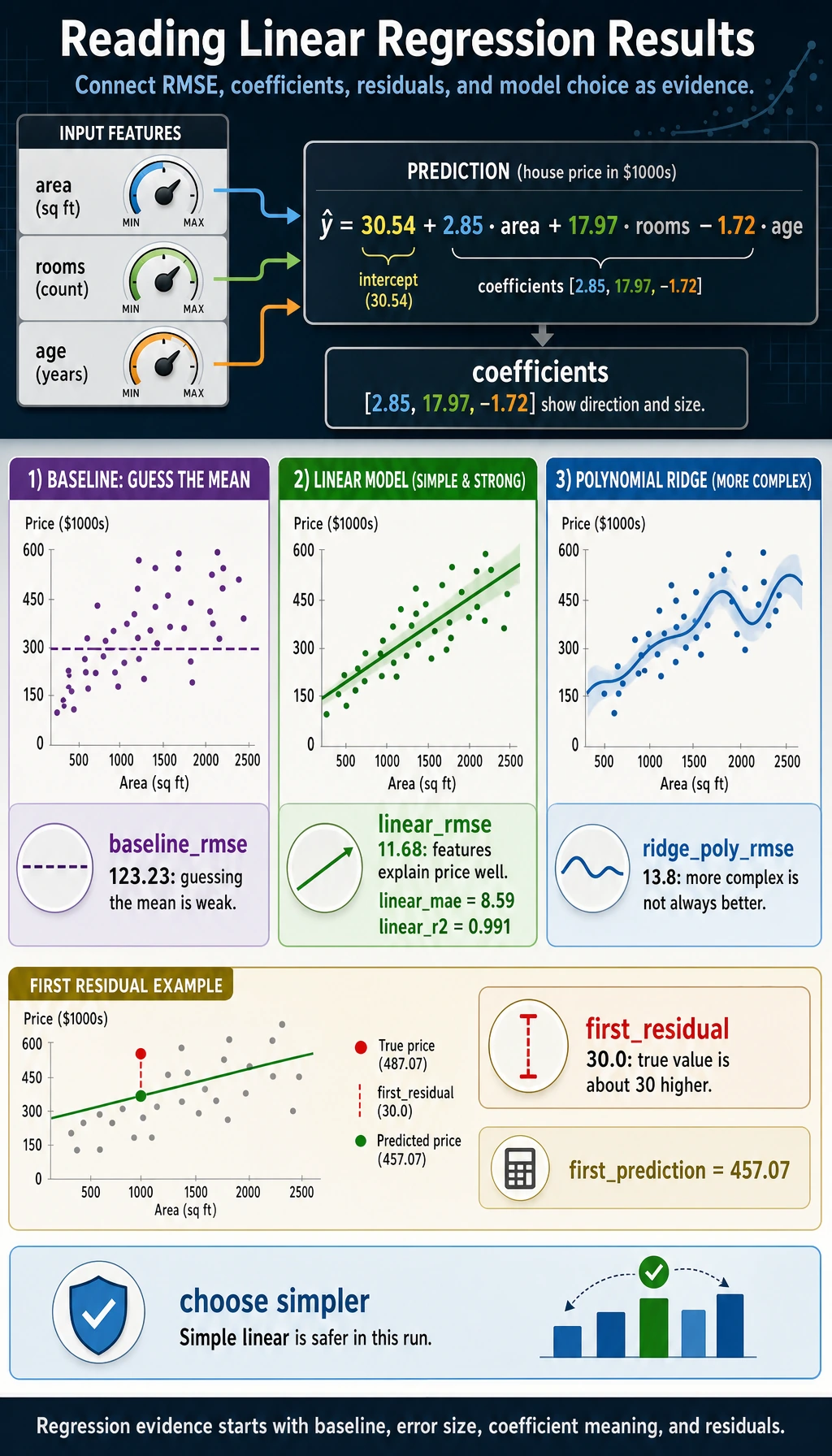

import numpy as npfrom sklearn.linear_model import LinearRegression, Ridgefrom sklearn.metrics import mean_absolute_error, mean_squared_error, r2_scorefrom sklearn.model_selection import train_test_splitfrom sklearn.pipeline import Pipelinefrom sklearn.preprocessing import PolynomialFeatures, StandardScaler

rng = np.random.default_rng(42)area = rng.uniform(45, 180, 80)rooms = rng.integers(1, 5, 80)age = rng.uniform(0, 30, 80)noise = rng.normal(0, 12, 80)price = 35 + 2.8 * area + 18 * rooms - 1.6 * age + noiseX = np.column_stack([area, rooms, age])

X_train, X_test, y_train, y_test = train_test_split( X, price, test_size=0.25, random_state=42)

baseline = np.full_like(y_test, y_train.mean())model = LinearRegression()model.fit(X_train, y_train)pred = model.predict(X_test)

print("baseline_rmse=", round(mean_squared_error(y_test, baseline) ** 0.5, 2))print("linear_rmse=", round(mean_squared_error(y_test, pred) ** 0.5, 2))print("linear_mae=", round(mean_absolute_error(y_test, pred), 2))print("linear_r2=", round(r2_score(y_test, pred), 3))print("intercept=", round(model.intercept_, 2))print("coefficients=", np.round(model.coef_, 2).tolist())print("first_prediction=", round(pred[0], 2))print("first_residual=", round(y_test[0] - pred[0], 2))

poly = Pipeline([ ("poly", PolynomialFeatures(degree=2, include_bias=False)), ("scale", StandardScaler()), ("ridge", Ridge(alpha=10.0)),])poly.fit(X_train, y_train)poly_pred = poly.predict(X_test)print("ridge_poly_rmse=", round(mean_squared_error(y_test, poly_pred) ** 0.5, 2))Run:

python ch05_linear_regression_lab.pyExpected output:

baseline_rmse= 123.23linear_rmse= 11.68linear_mae= 8.59linear_r2= 0.991intercept= 30.54coefficients= [2.85, 17.97, -1.72]first_prediction= 457.07first_residual= 30.0ridge_poly_rmse= 13.8

Read the Result

Section titled “Read the Result”The baseline predicts the training average for every house. Its RMSE is large, so the features matter.

The linear model learns a rule close to the hidden data recipe:

price ~= 30.54 + 2.85 * area + 17.97 * rooms - 1.72 * ageThat means, in this synthetic dataset:

| Feature | Learned direction | Interpretation |

|---|---|---|

| area | positive | larger houses cost more |

| rooms | positive | more rooms add value |

| age | negative | older houses cost less |

The first residual is 30.0, meaning the first test item was about 30 price units higher than the model predicted. One score is not enough; residuals tell you where the model is weak.

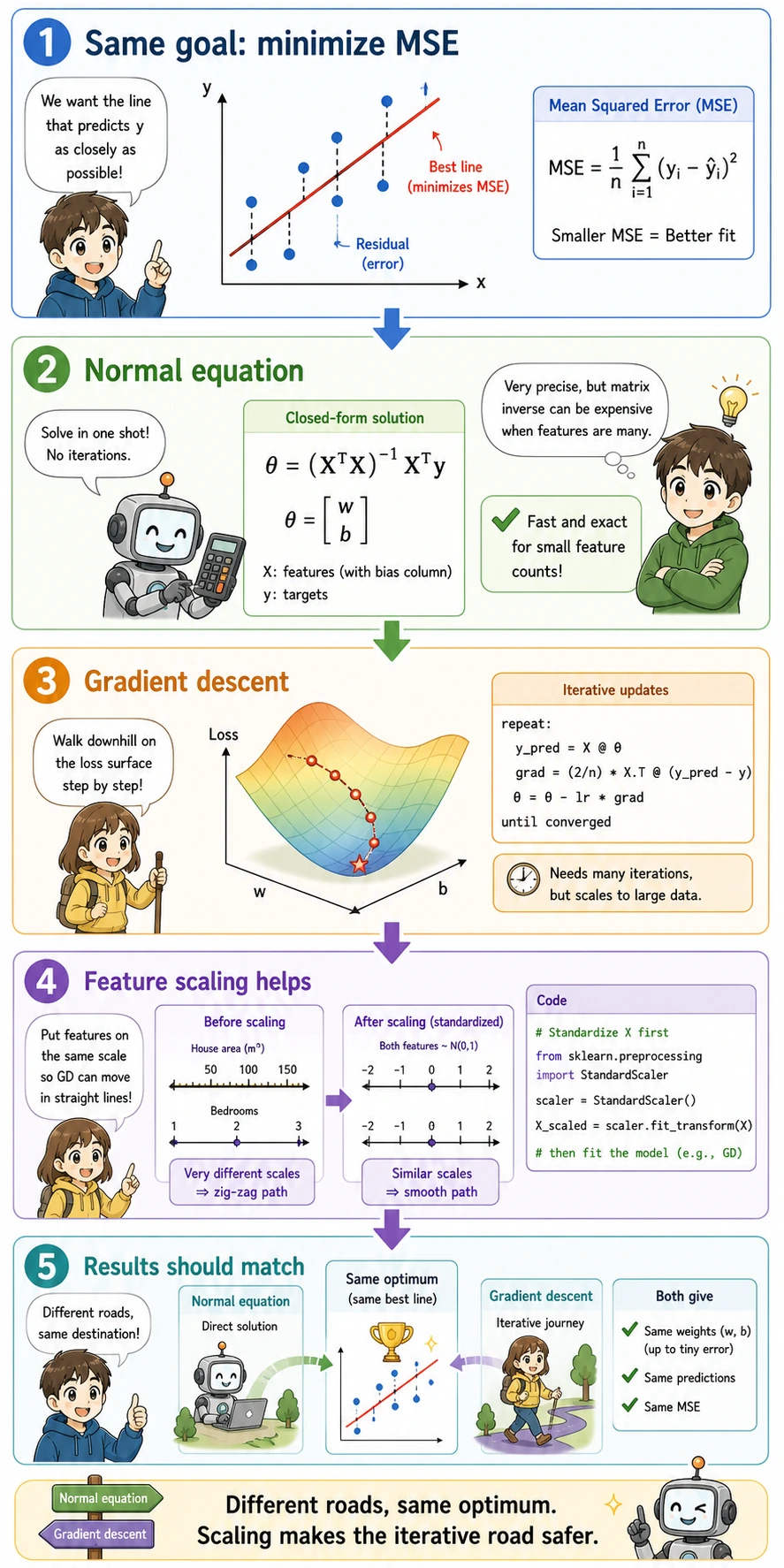

Solver Choice

Section titled “Solver Choice”

You do not need to hand-solve linear regression every day, but you should know the two ideas:

| Solver | What it means | When to care |

|---|---|---|

| normal equation / least squares | solve the best coefficients directly | small classic regression, theory intuition |

| gradient descent | improve coefficients step by step by lowering loss | large data, neural networks, custom objectives |

In daily sklearn work, call LinearRegression() first. Learn manual gradient descent to understand later neural networks, not because it is the default production implementation.

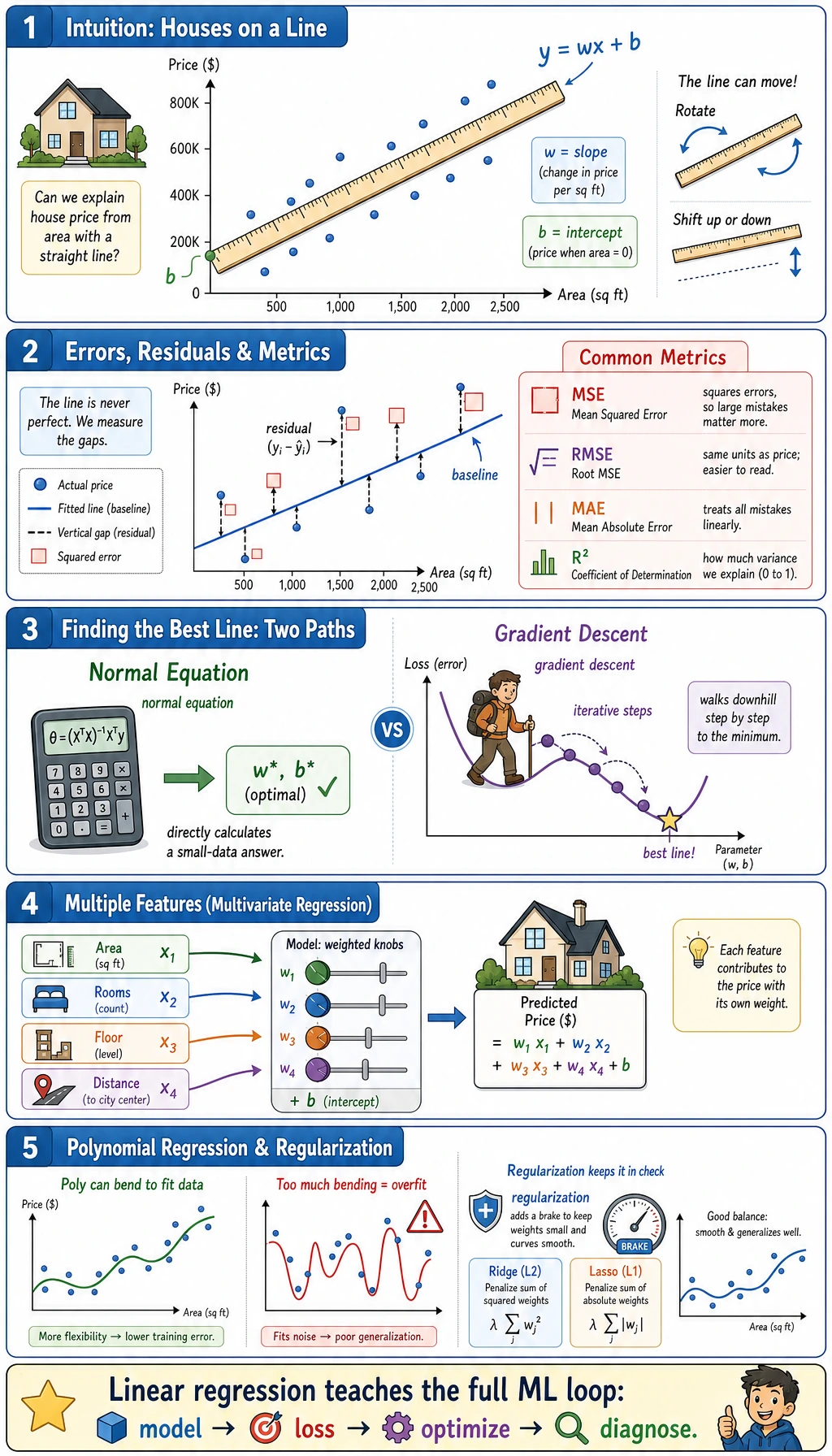

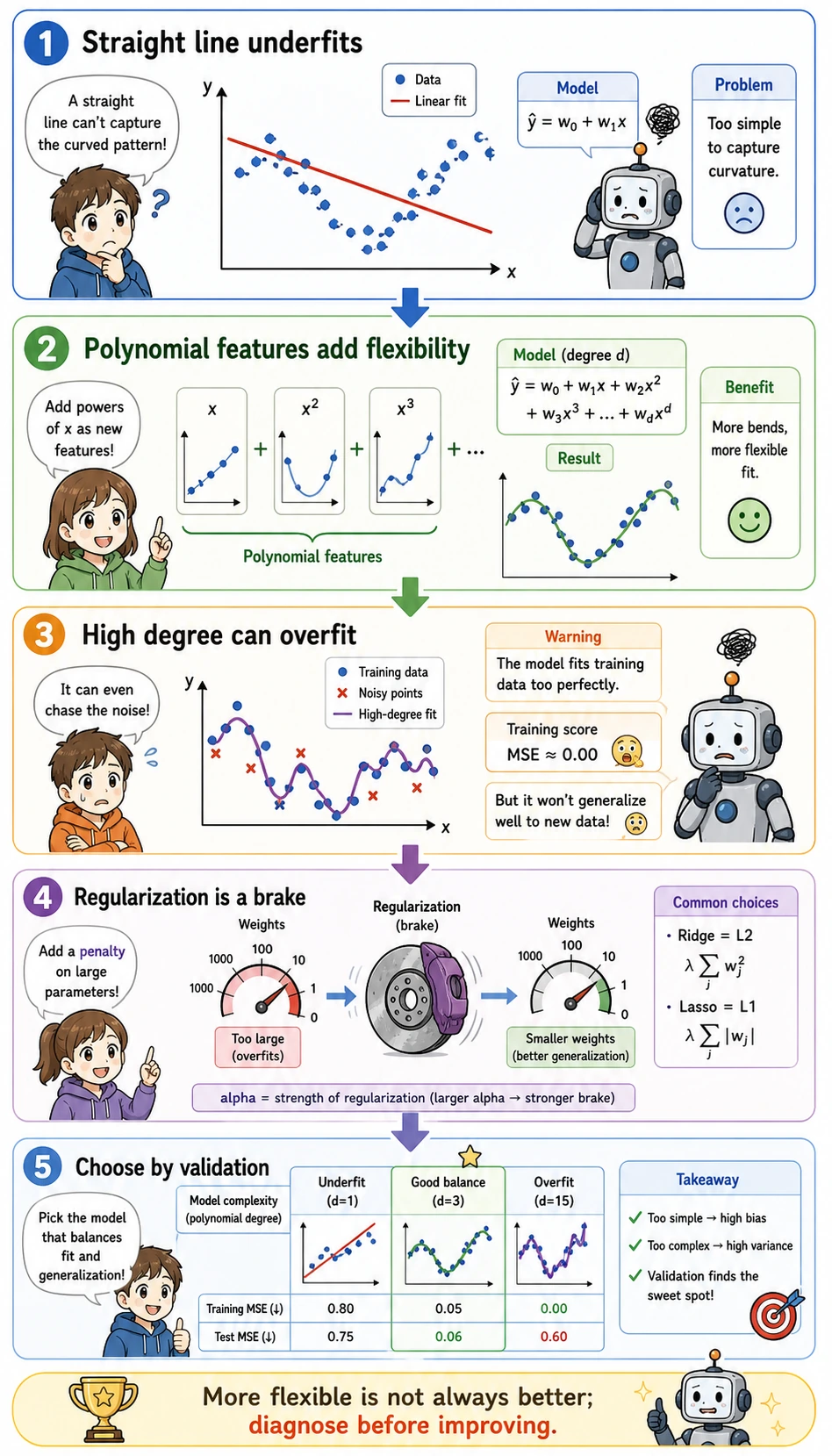

Polynomial and Ridge

Section titled “Polynomial and Ridge”

The script also tries:

This lets the model use interactions such as area * rooms, but Ridge adds a brake so the model does not bend too freely. In this synthetic run, polynomial Ridge is worse than the simple linear model, so the safer choice is the simpler one.

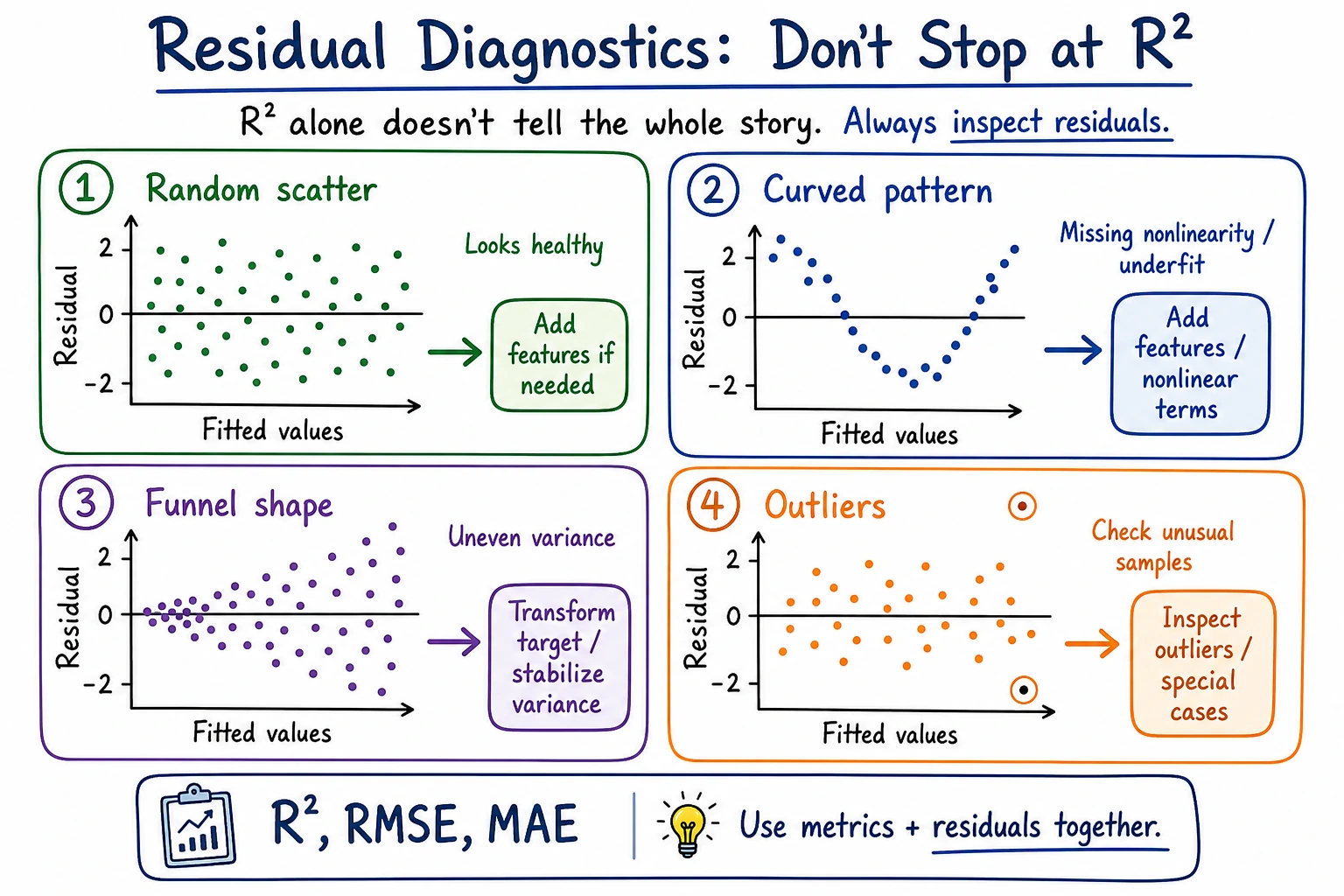

Check Residuals

Section titled “Check Residuals”

When a regression model looks good, still inspect residuals:

| Residual pattern | Meaning | Next action |

|---|---|---|

| random around zero | linear model may be enough | keep baseline and document result |

| curve shape | relationship may be nonlinear | try polynomial/features or another model |

| bigger spread at high values | error grows with target size | transform target or use robust metrics |

| a few huge misses | outliers or missing features | review rows and data quality |

Evidence to Keep

Section titled “Evidence to Keep”Keep this page’s proof of learning as a small evidence card:

- Task

- regression or classification problem with target definition

- Model

- linear/logistic/tree/ensemble/SVM configuration and train/test split

- Metric

- regression error, accuracy/F1, threshold curve, or confusion matrix

- Failure Check

- overfitting, underfitting, feature scaling, threshold choice, or class imbalance

- Expected Output

- model result plus error samples or residual review

Common Failures

Section titled “Common Failures”| Symptom | First check | Usual fix |

|---|---|---|

| model only slightly beats baseline | weak or wrong features | add useful columns, inspect correlations |

| great R² but bad individual cases | residuals hidden by average score | print largest residuals |

| coefficient signs feel wrong | feature leakage or correlated features | review columns and domain logic |

| polynomial model gets worse | overfitting or unstable scale | use Ridge and compare on test data |

| metrics are confusing | target unit unclear | report MAE/RMSE in business units |

Practice

Section titled “Practice”- Increase noise from

12to30and rerun. What happens to RMSE and R²? - Remove

agefromX. Does the error grow? - Change

Ridge(alpha=10.0)toalpha=0.1andalpha=100.0. - Save a short note with baseline RMSE, linear RMSE, best model, and one residual example.

Reference implementation and walkthrough

- More noise should increase RMSE and usually reduce R², because the target contains less predictable signal.

- If

agecarries useful information, removing it should increase error. If error barely changes, the feature may be weak or redundant with other columns. - Smaller

alphameans weaker regularization and coefficients can grow; largeralphashrinks coefficients and can underfit. - A useful note includes the naive baseline, each model’s metric, the chosen model, and one row with

actual,predicted, andresidualso the metric has a concrete meaning.

Pass Check

Section titled “Pass Check”You are ready for the next model when you can explain:

- why a baseline is needed before judging a regression model;

- how coefficients, intercept, prediction, and residual connect;

- why RMSE and MAE answer slightly different questions;

- when polynomial features help and when they overfit;

- why a simpler model can beat a more flexible one.